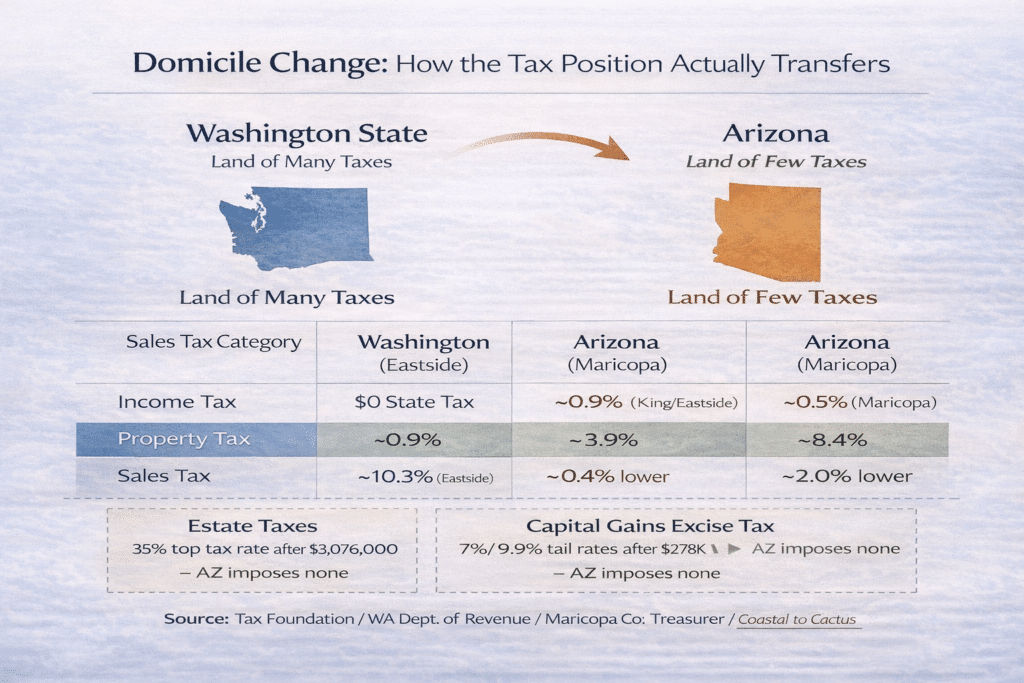

The tax comparison between Washington and Arizona is more complex than a single headline. Washington has no wage or salary income tax — but it does tax capital gains, and it imposes one of the steepest estate taxes in the nation. Arizona charges a flat 2.5% on all income, including wages and ordinary income from investments — but it imposes no estate tax, no capital gains tax, and no Real Estate Excise Tax on property transactions. The net result depends entirely on the household: its income level, its asset composition, its estate size, and how it deploys the proceeds from a home sale.

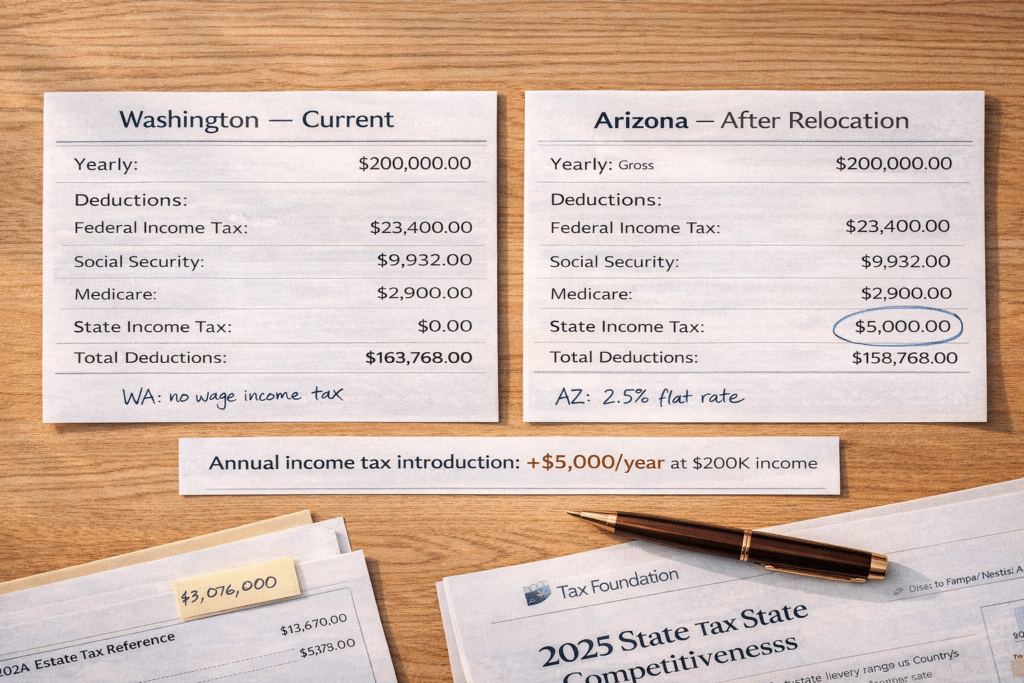

The most widely understood element of the Washington-Arizona tax comparison is also the most frequently mischaracterized. Washington imposes no tax on wages, salaries, or ordinary income. Arizona imposes a flat 2.5% on all taxable income. For a household whose income is entirely from wages, the difference is straightforward: every dollar earned in Arizona costs 2.5 cents in state tax that costs nothing in Washington.

| Income Tax Category | Washington | Arizona |

|---|---|---|

| Wages & Salary | 0% | 2.5% flat rate |

| Ordinary investment income (dividends, interest) | 0% | 2.5% flat rate |

| Social Security income | Not taxed | Not taxed at state level |

| Pension / retirement income | Not taxed | Not taxed by AZ for most retirement income |

Arizona Note: Arizona does not tax Social Security income at the state level. For households with significant Social Security or pension income, Arizona’s 2.5% applies to wages and investment income but not to those specific income streams, depending on the source. Consult a licensed tax professional for your specific retirement income composition.

$120,000 household income: +$3,000/year new cost in AZ

$200,000 household income: +$5,000/year new cost in AZ

$350,000 household income: +$8,750/year new cost in AZ

These figures are the gross income tax introduction — the annual cost of replacing Washington’s zero wage tax rate with Arizona’s 2.5% flat rate. They are real, recurring, and belong in every relocation financial model. They are offset, however, by the tax reductions detailed in subsequent sections — particularly property tax and, for applicable households, the elimination of Washington’s capital gains tax and estate tax exposure.

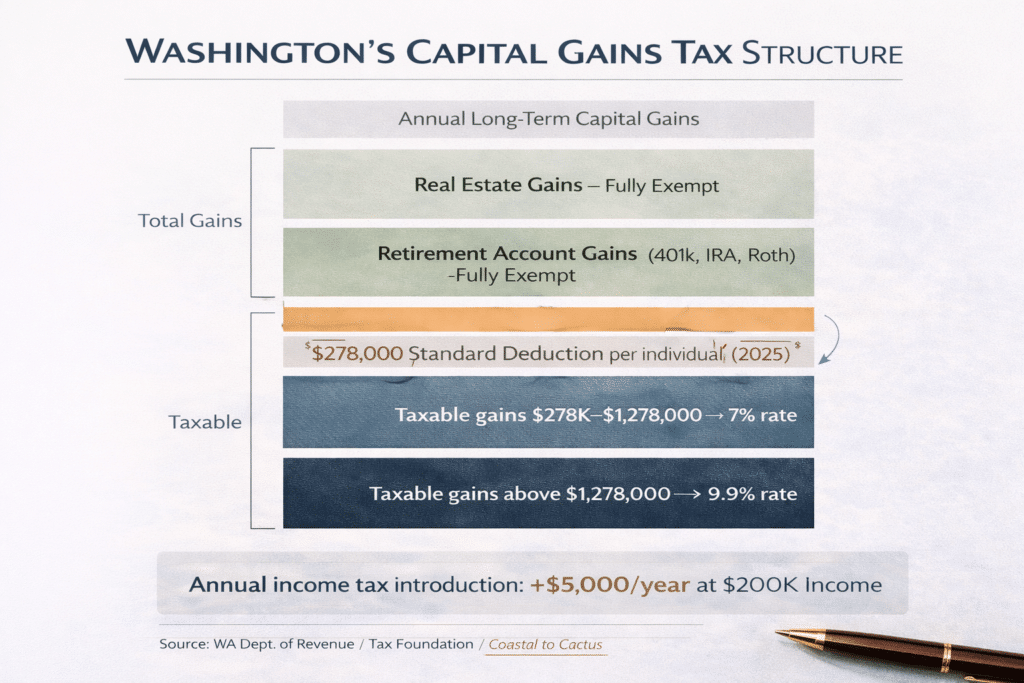

This is the part of Washington’s tax structure that surprises many homeowners. Washington doesn’t tax wages, but it does levy a capital gains excise tax on long-term gains from certain assets — including stocks, bonds, mutual funds, and some business interests. The structure took effect in 2022 and was expanded in 2025. Here’s how it works.

Washington Capital Gains Tax (effective 2025):

Standard deduction: $278,000 per individual per year (2025; inflation-adjusted annually by the WA Department of Revenue)

Rate on gains $278,001 to $1,278,000: 7%

Rate on gains above $1,278,000: 9.9% (new tier effective retroactively to January 1, 2025)

Critical exemptions — does NOT apply to:

Sales of real estate (primary residence, investment property, commercial — all real estate sales are exempt)

Qualified retirement accounts (401(k), IRA, Roth IRA)

Assets transferred at death

Qualified family-owned small businesses that meet statutory criteria

Home sale clarification: For the vast majority of Seattle-area homeowners, the sale of a Washington home is exempt from Washington’s capital gains tax. Washington’s REET (see Section 5) applies to the home sale — not the capital gains tax. A homeowner selling a $1,200,000 King County home owes no Washington capital gains tax on that transaction. The gain may still be taxable federally under standard capital gains rules (including the $500,000 federal exclusion for married filers if eligibility requirements are met), but Washington’s capital gains excise tax does not apply to the home sale.

The Washington capital gains tax most directly impacts households with significant stock, bond, or business interest gains above $278,000 per year. Households with a large concentrated stock position — common in King County and Eastside communities with technology company equity compensation — may have meaningful exposure to the 7% or 9.9% WA capital gains bracket. Establishing Arizona domicile before realizing those gains eliminates WA capital gains tax liability on those transactions (gains realized after establishing bona fide Arizona residency are not subject to Washington’s capital gains excise tax).

Arizona taxes capital gains as ordinary income at the 2.5% flat rate. Arizona also provides a 25% subtraction for qualifying long-term capital gains on assets acquired after December 31, 2011, from Arizona sources, producing an effective state rate of approximately 1.875% on those gains. For capital gains on most investment assets (stocks, bonds), Arizona’s treatment is:

| Asset Type | WA Capital Gains Tax | AZ Capital Gains Rate |

|---|---|---|

| Home sale | Exempt (REET applies instead) | Not applicable to WA home sale; AZ imposes no equivalent on AZ home purchases |

| Stocks / bonds (long-term) |

7% on gains $278K–$1.278M; 9.9% above $1.278M (after $278K standard deduction) |

2.5% (or ~1.875% on qualifying AZ-source LT gains) |

| Retirement accounts (401k, IRA, Roth) | Exempt (WA) | Not applicable; distributions taxed as ordinary income at 2.5% (AZ) |

Source: Washington Dept. of Revenue Capital Gains Tax page; Arizona Dept. of Revenue; Tax Foundation 2025; Keystone Global Partners Capital Gains Guide 2025

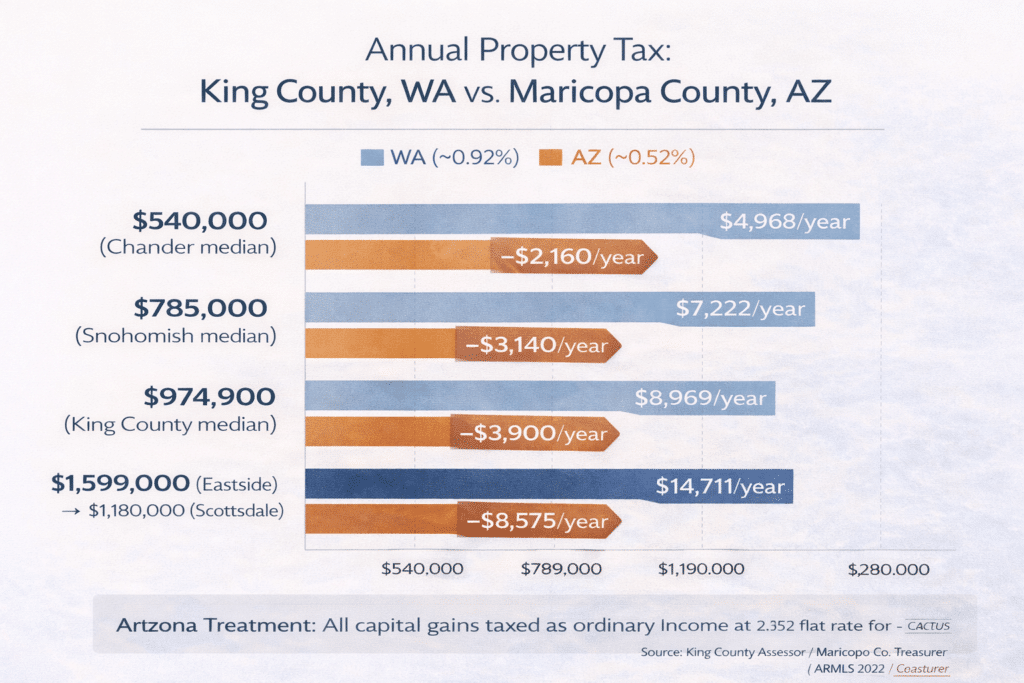

Washington and Arizona both impose property taxes at the local government level, with effective rates set by county assessors and taxing jurisdictions. The comparison between King County and Maricopa County is consistently favorable to Arizona across the historical record.

| Property Tax Category | King County, WA | Maricopa County, AZ |

|---|---|---|

| Effective tax rate | ~0.92% of assessed value | ~0.52% of assessed value |

| Assessed value basis | Market value at sale / periodic reassessment | Full purchase price at acquisition; periodic review |

| Prop 13 equivalent | None — WA has no Prop 13 equivalent; assessments can reset more freely | None — AZ has no Prop 13 equivalent; assessed value is 25% of full cash value (LPV) |

Source: Tax Foundation 2025; Maricopa County Treasurer; King County Assessor; Washington Dept. of Revenue

| AZ Purchase Price | WA Property Tax on Equivalent-Value Home | AZ Property Tax on AZ Purchase |

|---|---|---|

| $430,000 (Surprise/Goodyear) | ~$3,956/year (on $430K WA home at 0.92%) | ~$2,236/year ✓ ~$1,720/year savings |

| $540,000 (Chandler median) | ~$4,968/year (on $540K) | ~$2,808/year ✓ ~$2,160/year savings |

| $785,000 (Snohomish median as WA baseline) | ~$7,222/year (on $785K) (Snohomish seller equivalent) | ~$4,082/year (if purchasing at same value in AZ) |

| $974,900 (King County median as WA baseline) | ~$8,969/year (on $974.9K) (KC baseline) | ~$5,069/year ✓ ~$3,900/year savings on comparable value |

| $1,599,000 (Eastside median; Scottsdale purchase) | ~$14,711/year (on $1,599K) (Eastside baseline) |

~$6,136/year (on $1,180K Scottsdale purchase) ✓ ~$8,575/year savings |

Source: Calculations based on King County ~0.92% and Maricopa County ~0.52% effective rates; ARMLS / Phoenix REALTORS 2025 median prices

The property tax savings are the recurring annual benefit that most directly offsets the income tax introduction at moderate income levels. For Eastside sellers purchasing at or near the Scottsdale median, the property tax savings alone approach or exceed the income tax introduction at household incomes below $400,000. At higher income levels, the income tax introduction dominates — but the property tax savings remain persistent and cumulative over the holding period.

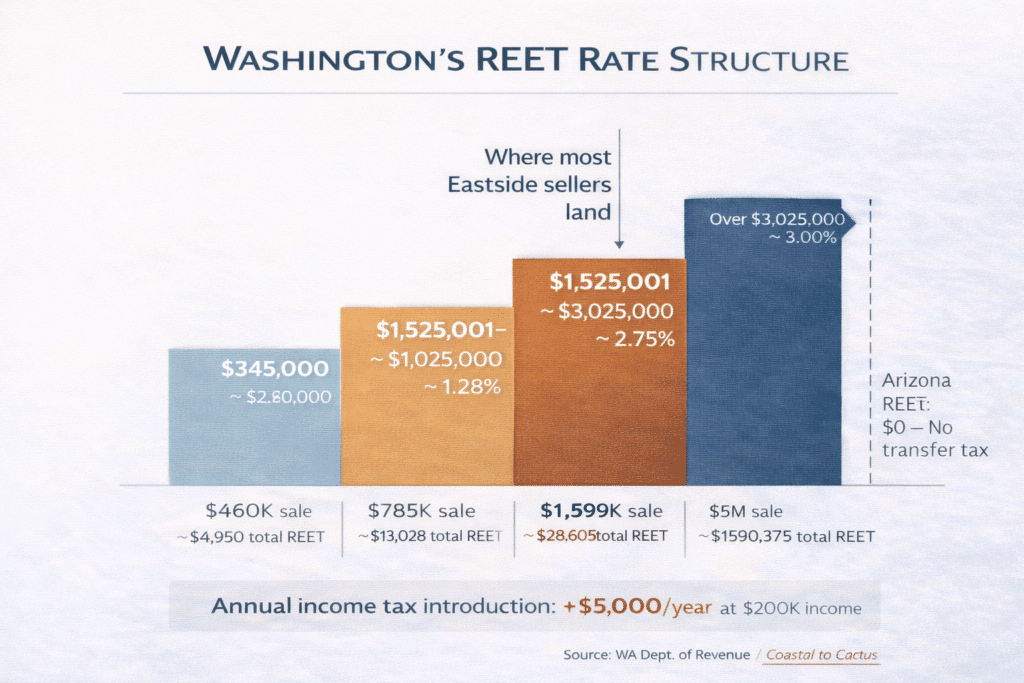

Washington imposes a Real Estate Excise Tax on every residential property sale. The tax is graduated, falling on the seller (though the buyer is liable if unpaid). Arizona imposes no equivalent transfer tax on real estate transactions.

| Sale Price Range | State REET Rate |

|---|---|

| $0 – $525,000 | 1.10% |

| $525,001 – $1,525,000 | 1.28% |

| $1,525,001 – $3,025,000 | 2.75% |

| Over $3,025,000 | 3.00% |

Source: Washington State Dept. of Revenue, REET Rate Schedule (current)

Plus: Local REET ranging from 0.25% to 0.50% depending on city/unincorporated area, collected in addition to the state REET rate above.

| Origin Market Median | Est. Total REET |

|---|---|

| Snohomish County ($785K) | ~$13,028 |

| King County ($974.9K) | ~$11,534 |

| Eastside Median ($1,599K) | ~$28,605 |

| Kirkland (~$2,190K) | ~$47,000+ |

| Mercer Island ($2,550K) | ~$59,500 |

| West Bellevue ($3,688K) | ~$98,155 |

REET is a one-time transaction cost paid at closing. It reduces net proceeds from the Washington home sale. Arizona imposes no REET, no transfer tax, and no equivalent exit cost on residential property transactions — making Arizona purchases marginally cheaper on a per-transaction basis compared to any equivalent Washington transaction.

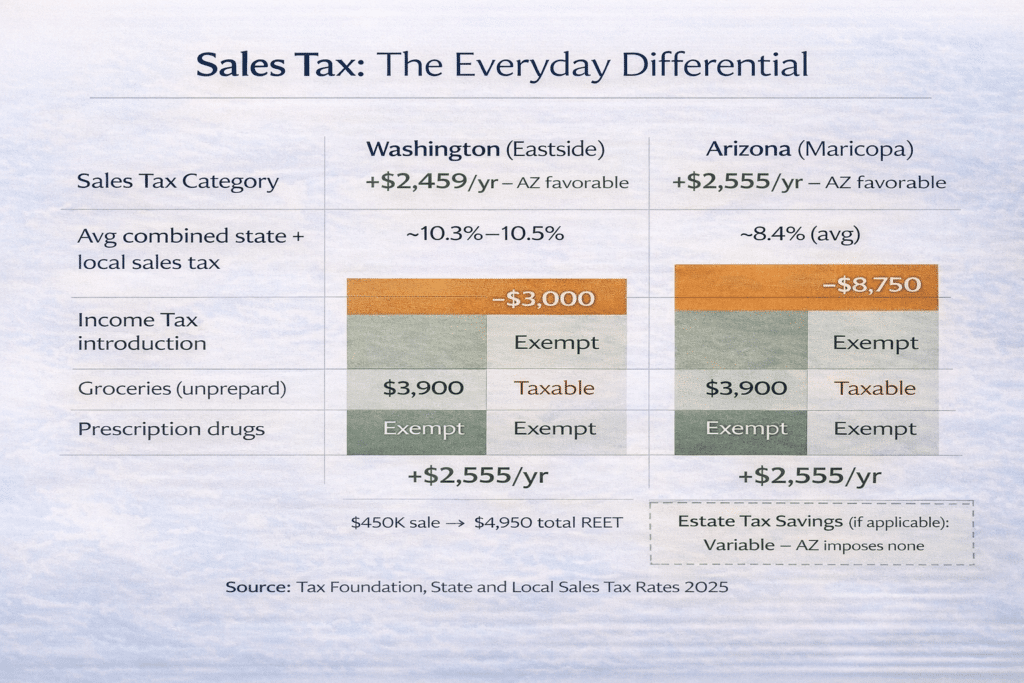

Washington and Arizona both impose combined state and local sales taxes. Neither imposes a sales tax on groceries (unprepared food). Washington’s rates are generally higher than Arizona’s across most cities and unincorporated areas.

| Sales Tax Category | Washington (Eastside) | Arizona (Maricopa) |

|---|---|---|

| Avg combined state + local | ~10.3%–10.5% | ~8.4% (avg) |

| Groceries (unprepared) | Exempt | Exempt |

| Clothing | Taxable | Taxable |

| Prescription drugs | Exempt | Exempt |

At $80,000 in annual taxable household expenditure — a reasonable estimate for an Eastside household — the 2.1-percentage-point differential produces approximately $1,680 per year in additional purchasing power in Arizona. At $55,000 in taxable spending, the savings are approximately $1,155.

The sales tax differential is persistent and cumulative, but it is the smallest annual item in the full Washington-Arizona tax comparison. Include it in your model — do not lead with it.

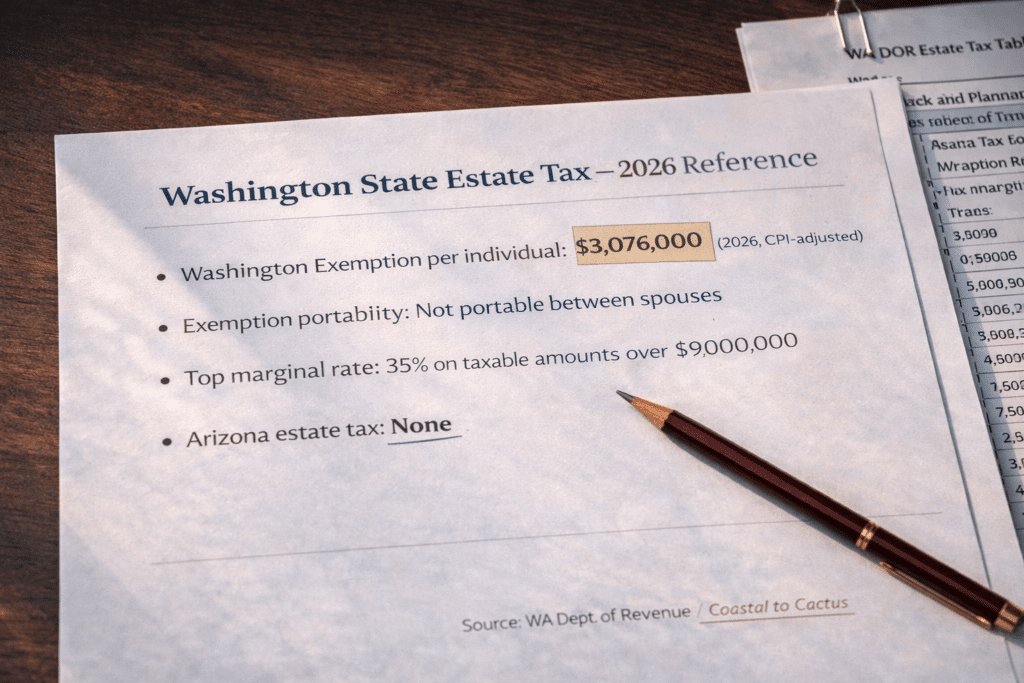

Washington is one of twelve states that impose a state-level estate tax independent of the federal estate tax. Arizona imposes no estate tax.

| WA Estate Tax Item | Pre-July 2025 (old) | Current (July 2025+) |

|---|---|---|

| Exemption per individual | $2,193,000 |

$3,000,000 (→ $3,076,000 for 2026, CPI-adjusted) |

| Top marginal rate | 20% (on estates over ~$9M) | 35% (on amounts over $9M) |

| Portability (spouses) | Not portable | Not portable |

| Annual inflation adjustment | Frozen since 2018 | Indexed to CPI (Seattle metro) |

Source: Washington Dept. of Revenue Estate Tax Tables (post-July 2025); DLO Law Group, January 2026; Perkins Coie 2025 Tax Update

Arizona imposes no state estate tax. Estates of any size passing to heirs under Arizona law are subject only to the federal estate tax (federal exemption: $15,000,000 per individual for 2026 per the One Big Beautiful Bill Act).

Rate table for the Washington taxable estate (overage above exemption):

| WA Taxable Estate Amount | Marginal Rate (post July 2025) |

|---|---|

| $0 – $1,000,000 over exemption | 10% – 14% (graduated) |

| $1,000,001 – $9,000,000 over exemption | 15% – 29% (graduated) |

| Over $9,000,000 over exemption | 35% (top rate) |

Source: WA DOR Estate Tax Table W (for deaths July 1, 2025 and after)

| Household Scenario | WA Estate Tax Exposure |

|---|---|

| Single individual, total estate < $3,076,000 | None — below $3,076,000 threshold |

| Single individual, Snohomish median home ($785K) + retirement + savings | Potentially exposed — depends on total net estate including retirement accounts, investment accounts, and other assets combined |

| Married couple, Eastside home ($1.6M) + retirement + savings | With proper trust planning, combined exemption ~$6,152,000. Without planning, surviving spouse may have single $3,076,000 exemption applied |

| Single individual, Mercer Island home ($2.5M) + investments > $3.076M | Material exposure. Taxable estate above exemption triggers graduated rates from 10%–35% |

| West Bellevue household, total estate > $9M | Significant exposure at top rates. Professional estate planning essential. |

A household that permanently relocates to Arizona and establishes Arizona domicile is no longer subject to Washington estate tax on intangible assets (stocks, bonds, retirement accounts held out of state). However, Washington estate tax continues to apply to real estate and tangible personal property physically located in Washington at the time of death — even if the owner is an Arizona resident. This means selling the Washington home as part of the relocation is not only financially motivated by equity release but also eliminates a potential Washington estate tax nexus for homeowners near or above the $3,076,000 threshold.

This is not legal or tax advice. Estate planning with respect to state domicile change requires counsel from a licensed estate planning attorney with knowledge of both Washington and Arizona law.

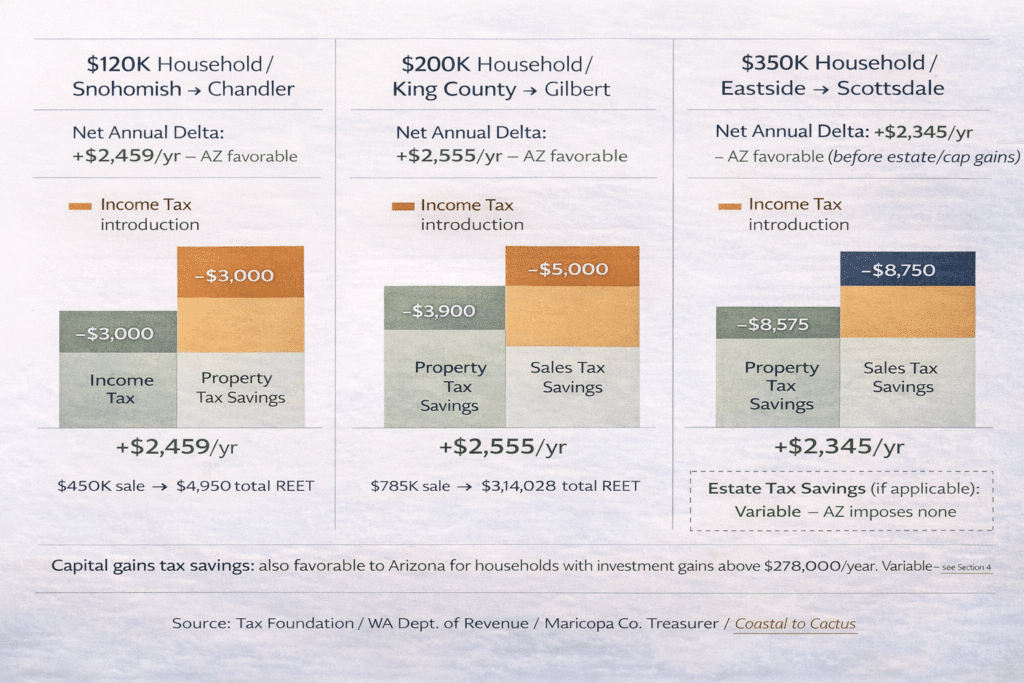

The following tables model the complete annual tax picture for three representative Washington-to-Arizona relocating households. All figures are estimates based on published rate schedules and approved data sources.

Model Assumptions: – Washington home sold; all tax exposure based on post-sale position – Arizona home purchased; property tax on AZ purchase price – Capital gains tax: excluded from annual model (one-time event; see Section 4) – Estate tax: excluded from annual model (future event; see Section 6) – Sales tax based on $55,000 annual taxable expenditure (Tier 1) / $80,000 (Tier 2) / $120,000 (Tier 3)

| Tax Category | Washington / Year | Arizona / Year | Delta |

|---|---|---|---|

| State Income Tax | $0 | +$3,000 | +$3,000 ⚠ |

| Property Tax | -$7,222 (on $785K WA) | -$2,808 (on $540K) | +$4,414 ✓ |

| Sales Tax | -$5,665 (10.3%) | -$4,620 (8.4%) | +$1,045 ✓ |

| Capital Gains | Potentially 7% on inv. gains >$278K | 2.5% (wages and ordinary income) | Favorable to AZ for inv. gains |

| Tax Category | Washington / Year | Arizona / Year | Delta |

|---|---|---|---|

| State Income Tax | $0 | +$5,000 | +$5,000 ⚠ |

| Property Tax | -$8,969 (on $974.9K) | -$3,094 (on $595K) | +$5,875 ✓ |

| Sales Tax | -$8,400 (10.5%) | -$6,720 (8.4%) | +$1,680 ✓ |

| Capital Gains |

7% on gains >$278K (applicable to inv. gains only; home sale exempt) |

2.5% on inv. gains (unless qualifying LT gains → 1.875%) |

AZ lower for large investors |

| Tax Category | Washington / Year | Arizona / Year | Delta |

|---|---|---|---|

| State Income Tax | $0 | +$8,750 | +$8,750 ⚠ |

| Property Tax | -$14,711 (on $1,599K) | -$6,136 (on $1,180K) | +$8,575 ✓ |

| Sales Tax | -$12,600 (10.5%) | -$10,080 (8.4%) | +$2,520 ✓ |

| Capital Gains |

7%–9.9% on gains >$278K (on inv. gains) |

2.5% on same gains (or ~1.875% on qualifying LT) |

AZ lower for large inv. events |

| Estate Tax |

Exposed above $3,076,000 / individual at 10%–35% rates |

None | AZ substantially favorable |

Most of the tax benefits in the Washington-to-Arizona comparison depend on establishing Arizona as your legal domicile — your primary and permanent home. This is not automatic at the moment of home purchase. It requires active steps.

What Washington taxes after you move:

Washington can continue to tax a former resident if domicile is not properly established in the new state. California and New York are known for aggressive residency audits; Washington is generally less aggressive, but the risk is real for high-income households with continued Washington-source income or property remaining in Washington.

Washington’s capital gains tax applies to gains realized by Washington-domiciled individuals. A household that sells stock in January and moves to Arizona in June may be subject to Washington capital gains tax on gains realized before the domicile change date. Timing of major asset sales relative to the domicile change date is a significant planning variable.

Washington estate tax continues to apply to real property located in Washington, regardless of where the owner is domiciled at death. Selling the Washington home eliminates this nexus.

Steps to establish Arizona domicile:

Arizona domicile is generally established by demonstrating that Arizona is your primary and permanent home. Evidence typically includes: – Purchasing Arizona real property as primary residence – Registering vehicles in Arizona – Obtaining an Arizona driver’s license – Registering to vote in Arizona – Updating financial accounts, estate documents, and correspondence to Arizona address – Spending the majority of days in Arizona

For households with significant stock equity compensation (RSUs, options, long-term positions), the date of Arizona domicile establishment may meaningfully affect Washington capital gains tax liability. Gains realized after Washington domicile is terminated are not subject to Washington’s capital gains excise tax. Professional tax counsel on timing is strongly recommended for households with expected capital gains above $278,000 in the year of the move.

This is not legal or tax advice. Domicile planning requires consultation with a licensed attorney and tax professional familiar with Washington domicile law.

| Tax Category | Washington State | Arizona (Maricopa Co.) |

|---|---|---|

| State Income Tax (wages) | 0% on wages/salary | 2.5% flat on all taxable income |

| State Capital Gains Tax |

7% on gains $278K–$1.278M; 9.9% above $1.278M

(after $278K standard deduction); real estate EXEMPT |

2.5% (or ~1.875% on qualifying LT gains); real estate not separately taxed (taxed as ordinary income) |

| Effective Property Tax Rate | ~0.92% (King County) | ~0.52% (Maricopa Co.) |

| Real Estate Excise Tax (on home sale) | 1.10%–3.00% (graduated state); + local ~0.50% | None |

| Avg Combined Sales Tax | ~10.3%–10.5% | ~8.4% |

| Estate Tax |

Yes — $3,076,000 exemption (2026); 10%–35% graduated; NOT portable between spouses; top rate 35% (on amounts over $9M) |

None |

| Social Security Tax | Not taxed | Not taxed |

| Inheritance Tax | None | None |

| Capital Gains on Home Sale (state level) | Exempt (REET applies) | N/A; no equivalent WA-style CGT on AZ home purchases |