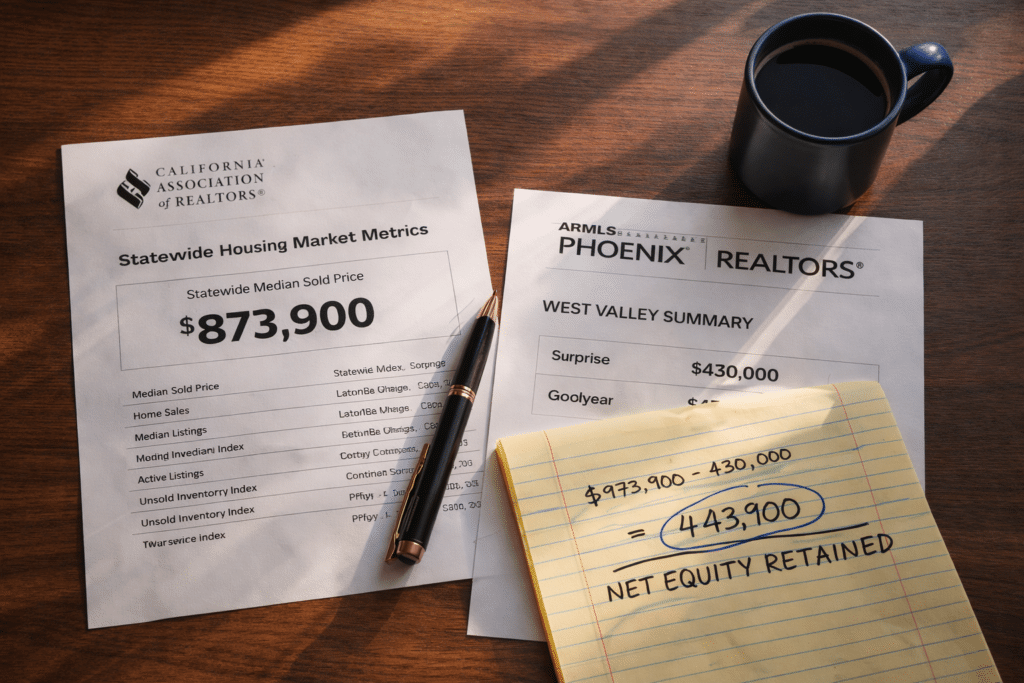

In Surprise, the 2025 median single-family home closed at $430,000. In Goodyear, it was $475,000. Against California’s statewide median of $873,900, that gap isn’t a different neighborhood — it’s a different balance sheet. Among Phoenix Valley destinations, the West Valley consistently produces the highest retained equity for California sellers after the transaction closes.

The West Valley sits at the low end of the Phoenix Valley price stack the zone where California equity goes furthest. That is a pricing function, not a narrative: even after multiple years of strong appreciation, Surprise and Goodyear remain below East Valley medians.

A California seller at the statewide median of $873,900 who purchases in Surprise at $430,000 retains approximately $380,000 to $420,000 in net equity after standard transaction costs on both ends. A Goodyear purchase at $475,000 retains roughly $330,000 to $370,000. These outcomes are the highest net-equity retention available in the Valley for a median California sale. Gilbert, Chandler, and Scottsdale produce different tradeoffs but they do not produce more retained equity than a West Valley purchase at the median.

That retained equity is not theoretical. A seller retaining ~$400,000 can eliminate the new mortgage entirely or deploy the capital to reduce the payment dramatically. At 6.5% with 20% down, a $430,000 purchase models near $2,175/month in principal and interest often a $2,000+ monthly reduction relative to California housing costs at comparable equity levels. Over ten years, that monthly delta compounds into material wealth.

Arizona’s tax structure compounds the outcome. Arizona’s flat 2.5% income tax versus California’s top marginal 13.3% can produce $15,000 to $20,000 in annual state income tax savings for a $200,000 household. Maricopa County’s effective property tax rate (~0.52%) applies to the full purchase price: roughly $2,200/year on a $430,000 Surprise purchase and about $2,500/year on a $475,000 Goodyear purchase. California’s Prop 13 protection ends at sale; the next home is assessed at full purchase price wherever it is purchased.

The West Valley is a development corridor anchored by Surprise and Goodyear, with adjacent growth in Buckeye, Avondale, and Peoria. For California equity analysis, Surprise and Goodyear function as the core destination markets, each with distinct inventory patterns and median price profiles.

Surprise posted year-to-date closed sales growth of 7.4% in 2025, with new listings up 14.1% through year-end 2025 (Phoenix REALTORS / ARMLS reporting). The median settled at $430,000, down modestly from $436,000 the prior year. Days on market increased from 72 to 80, consistent with broader market normalization. Months’ supply rose to about 4.2 months, indicating more negotiating room than peak-cycle conditions.

Goodyear’s 2025 profile was driven by volume: closed sales climbed 27.2% year-over-year through October. The median ran around $475,000 on a 10-month basis with modest moderation from the prior year. Average days on market rose to 75 from 68, and new listings were up 16.9%, expanding buyer choice versus earlier cycles.

Both markets skew toward newer construction (often built within the last 10–20 years) and floor plans that run larger than older, established-infill markets at comparable price points. A significant share of inventory is associated with master-planned development along the Loop 303 and I-10 corridors, which supports newer systems, newer rooflines, and larger standard footprints.

Year-over-year increase in closed sales in Goodyear through October 2025

The table below maps a median California sale ($873,900; estimated net proceeds after 6% transaction costs: ~$820,000) against major Phoenix Valley destinations by median price and estimated equity retained.

The West Valley’s advantage is structural: lower medians produce higher retained equity. Surprise and Goodyear sit further from several established East Valley employment corridors, representing a geographic tradeoff that some California sellers can make based on work structure, commute tolerance, or post-work income planning.

| Community | Median Price (2025) | Est. Equity Retained | Profile |

|---|---|---|---|

| Surprise | ~$430,000 | ~$345K–$390K | Maximum retained equity; newer inventory mix |

| Goodyear | ~$475,000 | ~$295K–$345K | Strong volume growth; newer builds on larger lots |

| Mesa | ~$490,000 | ~$280K–$330K | Broad inventory range; established + infill |

| Chandler | ~$540,000 | ~$230K–$280K | Tech corridor proximity; established neighborhoods |

| Gilbert | ~$595,000 | ~$175K–$225K | Master-planned; strong HOA infrastructure |

| Scottsdale | ~$1,180,000 | Premium positioning | Valley’s highest-priced market; luxury-tier deployment |

Price data: Phoenix REALTORS/ARMLS 2025 YTD. Net equity estimates assume 6% transaction costs on California sale plus standard Arizona closing costs. Estimates only.

The California-to-West Valley gap doesn’t only produce retained capital — it converts into square footage. Median West Valley inventory commonly lands in the 2,000 to 3,200 sq ft range on lots often 6,000 to 12,000 sq ft, frequently with three-car garage configurations. This physical product rarely exists at comparable price points in California coastal markets.

Example trade: a ~1,400 sq ft LA County home may close near $890,000, while a ~2,600 sq ft Surprise home on an ~8,500 sq ft lot can close near $430,000–$460,000. The California seller can unlock retained equity, reduce monthly housing cost by ~$1,800–$2,300, and acquire materially more interior area. Cost-per-square-foot is the cleanest expression of what California equity converts to in the West Valley.

New construction supply can further compress monthly costs through builder incentives (rate buydowns and closing cost contributions), particularly as market competition normalizes.

Approximate cost per square foot in Surprise and Goodyear (ARMLS 2025 YTD), versus $600–$900 per sq ft in major coastal California markets

Arizona’s income tax advantage is statewide and does not vary by Phoenix Valley community. The West Valley’s lower purchase price reduces the property tax bill further in absolute dollars.

A household selling in California, purchasing a $430,000 home in Surprise, and earning $200,000 can capture roughly $9,300 to $12,500 in combined income and property tax savings in year one versus California. Over ten years, cumulative savings can approach $100,000+, separate from equity retained at closing.

| Tax Category | California (Statewide) | Arizona (Maricopa Co. / West Valley) |

|---|---|---|

| Top State Income Tax Rate | 13.3% (+ 1.1% surcharge) | 2.5% flat |

| Effective Property Tax Rate | ~0.73% | ~0.52% |

| Annual Property Tax on $430K Home | ~$3,139 | ~$2,236 |

| Annual Property Tax on $475K Home | ~$3,468 | ~$2,470 |

| State Income Tax on $200K AGI | ~$14,300–$17,500 | ~$5,000 |

Sources: Tax Foundation 2025; Maricopa County Treasurer; California Franchise Tax Board

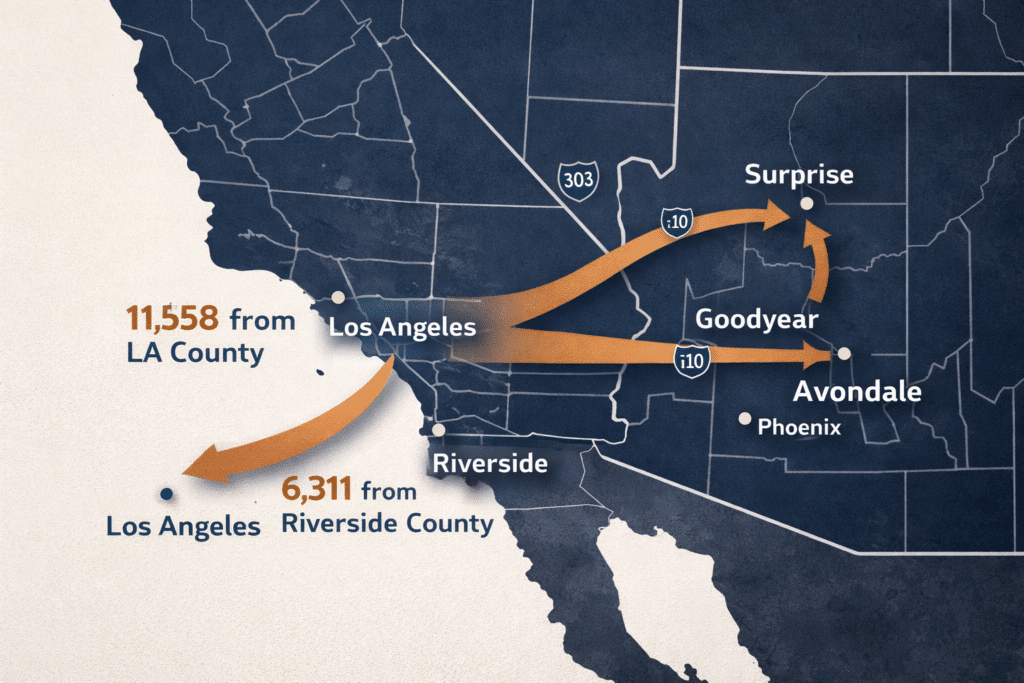

The West Valley’s growth as a destination for California equity buyers is documented in IRS county-to-county migration flows and supported by change-of-address dynamics. Riverside County sent 6,311 tax filers to Arizona in the 2021–2022 IRS filing year. Los Angeles County sent 11,558. The West Valley’s Loop 303 and I-10 corridors sit roughly a 5–6 hour drive from Inland Empire and LA origin points — a friction threshold that tends to correlate with deliberate, math-driven moves rather than casual churn.

IRS income-bracket data shows growth in the $100,000–$200,000 bracket outpacing lower bands. These are households with equity positions large enough to benefit from the West Valley retention math: sell, buy below East Valley medians, and redirect the retained capital into mortgage elimination, reserves, or investment.